|

|

|

|

|

4/2 – Is the SolarCity Model the Only Way to Scale Residential Solar? Wednesday, April 2nd 2014 From Greentechmedia: Is the SolarCity Model the Only Way to Scale Residential Solar? The U.S. residential solar market is growing rapidly and undergoing a major transformation at the same time. A new acquisition, partnership, or project fund seems to be announced every week. But what is the underlying trend here? For a while, many of us simply boiled it down to industry consolidation. The most recent developments, however, point to something even more specific: vertical integration.

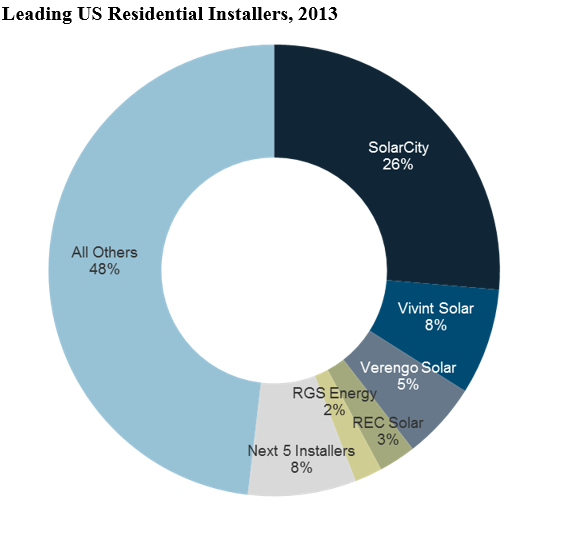

Follow the leader SolarCity and Vivint Solar, the top two residential installers in the U.S., installed more than one-third of all residential systems in 2013 and raised more than half of the $2.3 billion in project funds announced last year. (We’ll discuss more finance trends in an upcoming update to last year’s U.S. Residential Solar PV Financing report.) The two companies have very different strategies, especially when it comes to acquiring customers. Vivint is known for selling exclusively door-to-door, while SolarCity has a diversified approach that includes retail partnerships, cold calling, advertising, and anything else you could think of. However, there are two key similarities between these installers: they both primarily offer third-party owned solar (leases and PPAs), and they are the only two national, completely vertically integrated residential solar companies. Across these and other finance providers, the TPO model has proven easy to scale given the large addressable market of consumers who can afford a lease but not the purchase of a system. But does having control of both the project funding and installation give SolarCity and Vivint an additional advantage over their competitors? Read the rest on Cleantechmedia. |

News & Updates

Calendar

|

|

Smart Energy Initiative • Chester County Economic Development Council

Eagleview Corporate Center • 737 Constitution Drive • Exton, PA 19341 • 610-458-5700 • Fax: 610-458-7770 |

|